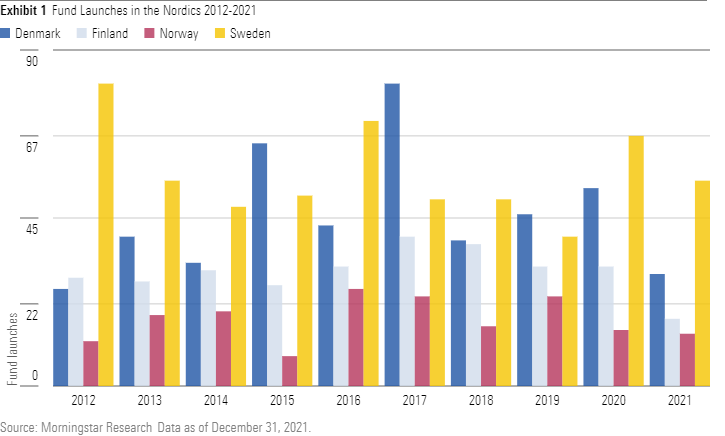

Morningstarin John Rekenthaler taustoittaa taktisen allokaation historiaa ja tehokkuutta. Aiemmin yhdistelmärahastojen joukossa oli "ajoitusrahastoja" jotka pyrkivät käteisen ja osakkeiden välisellä tasapainolla pärjäämään markkinoita paremmin, mutta harva onnistui siinä. Nyttemmin ajoitus tehdään usein hienovaraisemmin ja useamman omaisuuslajin avulla, mutta edelleen moni salkunhoitaja uskoo pystyvänsä ajoituksella synnyttämään lisäarvoa. Rekenthalerin mielestä todistustaakka on edelleen salkunhoitajilla, sillä tulokset eivät ole aina mairittelevia. Tyypillistä on myös, että taktista allokaatiota harjoittavat rahastot tulevat myyntiin usein vasta kriisin jälkeen, kun edessä on tyypillisesti pitkä osakenousu, jossa ne eivät pärjää erityisen hyvin.

Jason Stipp: I'm Jason Stipp for Morningstar. On the heels of Lehman's collapse five years ago, buy-and-hold investing took a hit along with investors' portfolios, while tactical investing or market-timing strategies came to the forefront.

Here to talk about how those strategies have played out is Morningstar's vice president of research, John Rekenthaler.

John, thanks for being here.

John Rekenthaler: Thank you, Jason.

Stipp: You've been at Morningstar a long time. You've covered a lot of different kinds of funds. You've covered market-timing funds in the '80s and in the '90s. So, you have a lot of experience with these funds and their strategies and how they've played out. Give us a little bit of a history on these funds, when they've come out, and what you've learned from covering them?

Rekenthaler: To start, there aren't really any funds that call themselves "market timing" anymore in a purest sense, but these were quite popular when I started at Morningstar in 1988. Market-timing fund being defined as a fund that has an on/off switch, either they're basically in stocks, fully in stocks, or they're out of stocks, depending upon a signal that they get.

These used to be quite popular. The reason that they're not popular anymore is they universally failed, and you can't find them because it didn't work. In particular, they did operate in a tough environment for them in the 1990s, which had a long bull market, and they had too many "off " signals during the bull market, so that pretty much killed them off.

However, the cousins of market-timing funds, or I suppose you could say successors, would be funds that are now called tactical allocation, or names like that. They're not usually on/off, 100% stocks to 0% stocks. It's more nuanced than that, which gives them less room to get into trouble, but they still face some of the same issues.

Stipp: They're able to shift their portfolios, in some cases pretty dramatically, depending on where they're seeing opportunity and where they're seeing risks.

Rekenthaler: That's right. It's not just stocks or cash, which the market-timing funds were. It might be stocks, cash, bonds, various international securities. So they do a lot more than the old market-timing funds. They have much more flavor to them, or variety to them.

Stipp: You said that so-called market timing funds aren't really around anymore under that label. What happened to them? You said they hit some tough times. Why weren't they able to succeed? What were the issues behind them and why did investors eventually leave them?

Rekenthaler: Well, the issue with market-timing strategies, and by this I mean very broadly, not just the old market-timing funds, but the new tactical allocation funds and the notion that buy-and-hold is dead, which came out after 2008. In 2009 I was attending conferences, and I kept getting questions about, is buy-and-hold is dead, or a statement that buy-and-hold is dead as a fact, [and] how should we run our portfolios knowing that to be true?

So, all of these concepts from market-timing, to buy-and-hold is dead, to tactical allocation, the notion being that you could adjust your stock market exposure depending upon conditions. These things tend to work pretty well--they do work well--when you do run into a stock market crash, the kind of thing that happens maybe once every decade or so. They do protect on the way down, because these signals, what happens is they almost all work the same. You sit out part of a decline or you sit out a good amount of a decline before they announce that a trend is going on, and then they get you out. In a routine bear market, the problem is, they get you out near the bottom, because you drop about 10% or so, and then the signals click and say get out, and then the market comes back. But in a crash, they do work. These people were out early fairly early in 2008. They got out on the way down in the October 1987 market crash. They got out during the early 2000s technology crash on the way down. It's getting back into the market that's a problem.

Stipp: Also isn't it the case that a lot of these funds aren't necessarily around before a market crash happens? It's after a market crash that everyone wants protection that you start to see more of them crop up?

Rekenthaler: I was making the generous assumption that somebody actually owned those funds before a market crash happens, but the problem is the market crash tends to happen after a long period of stock market growth--after a bull market. Logically, the best time to be in a market-timing fund is at the top of a market or after stocks have appreciated a lot, but it's the reverse that happens. People tend to be less attracted to risk-averse funds as the bull market continues, and they go to more aggressive funds or they go to funds that are fully invested. So they don't play at all well into investor psychology, and they tend not to be used well.

That's a different issue. I'm glad you raised it, but it is a different issue. Even the funds that are able to exist, and there aren't many of them, over a couple of market cycles, they still tend not to do very well. They're hard to hold, but even if they exist, they don't do very well just on paper returns, because they tend to miss the upside. They do dodge the big downside, but they miss the upside.

Stipp: You said these funds tend to have trouble knowing when to get back in. Since 2008, how have we seen the newest breed of these tactical asset allocation funds perform? Have we seen them not be able to really keep up because of that problem you mentioned?

Rekenthaler: You can say, John, it's a little unfair to point at these funds and say they haven't been able to keep up with a roaring bull market, where stocks have more than doubled since March 2009. They can't be expected to keep up with it. This is the worst possible environment for them from a relative basis. The problem is, that's when they were opening up, as you mentioned, and asking for assets and attracting assets, and when they were most appealing to investors was at the time that was worst to own them--after a market crash.

Stipp: You have said that the way that these funds are sold often is under a certain argument about why it's necessary to have one of these funds at this time. Essentially they'll always say it's different this time; buy-and-hold won't work anymore. So you need to have something that's more tactical and can get in and out of the market.

What about that argument? How does that sound to you now given that we've seen the recovery since 2008, that it's different this time? Can we say that it's really not different this time, or do we know yet?

Rekenthaler: I think we could fairly say it's not different this time, and in fairness, I was wondering this in 2009 myself when I got these questions about, is buy-and-hold dead. I'd say, I don't think so. When I got the statement, buy and hold is dead, what should we do differently? I would ask back, why is 2009 different than 2007 or 1999 or 1989 or 1979? Yes, we just did have a terrible crash in 2008, one that, of course, I didn't anticipate and I was surprised by that, shocked by that, my portfolio was hurt by that, I didn't enjoy it, etc. But that didn't mean that the rules were now different.

I really think that it was an emotional response, the notion that this time is different, that people were not able to distance themselves from the true shock and surprise that almost all of us had. It became something that sounded appealing. It felt like the right thing to do. It felt like it was prudent now after this crash that was just so different than anything that had happened in the market. It was much worse than 1987, which I had been around for. You have to go back to the early 1970s. So really it was 35 years before that previously had we encountered something as rocking and shattering as [2008]. I think when you step back, and we're able to do so now four years later or little more, and look at it dispassionately and say, where did that come from? Where is the defense for that? Why would the strategies that worked throughout our lifetimes … stop working at that period in time?

Stipp: John, I think the other issue with saying buy-and-hold is dead is that buy-and-hold means different things to different people. I've heard Scott Burns from Morningstar often say the missing element when you talk about buy-and-hold that's actually often used in practice is buy-and-hold, and also rebalance. So that, in a sense, when you're rebalancing, you are selling some of the winners, you are buying some of the losers, what Christine Benz calls "tactical-lite," but that rebalancing piece, which is so often part of a buy-and-hold investors' process, isn't part of that buy-and-hold statement usually when it's mentioned by itself.

Rekenthaler: That's a good point. I'm using it in fairly general terms. Buy-and-hold with rebalancing is really what I do intend, and that's the preferable way to do it. But frankly, buy-and-hold without rebalancing is a whole lot better, in my view, than when you get away from buy-and-hold and you start to get into the notion of, I am really going to adjust my portfolio's stock exposure in a top-down and mechanical, signal-driven way, because I think I can outsmart the market in doing that.

If somebody can do it, and they can have a public track record, let them do it. I haven't seen it. So, that would be a fund purchase that would have to be done on faith, and I don't think we should be bringing faith into our investments. [Faith is for] other places.

Stipp: All right, John. A very interesting history lesson and context on buy-and-hold investing versus the many different types of market-timing and asset allocation strategies we've seen over the years. Thanks for joining me.

Rekenthaler: Thank you, Jason.

Stipp: For Morningstar, I'm Jason Stipp. Thanks for watching.